Allocating Capital: Cash

The smartest investors I know make every dollar, pound, or yen work as hard as possible for them. Some of the biggest mistakes I see a lot of investors make regards how they treat their cash.

Cash is great, it’s the only asset you can easily and directly buy things with.

Cash sitting in your accounts actually serves three very distinct practical jobs:

- Working capital - available for payments at the moment funds are needed

- Operating reserves - available to satisfy upcoming expected or unexpected expenses

- Investing reserves - available to deploy into investment opportunities (unexpected) or meet upcoming capital calls (expected pre-committed investments)

Cash, in stable economies, also serves another, absolutely critical, psychological job. Cash has low volatility - so when the world goes upside down and asset prices crash, credit markets seize up, interest rates spike - cash is your best friend. This makes cash like a comforting safety blanket.

Cash has the reputation of being safe, but there are actually a surprising number of ways to screw things up with this asset class.

Problem 1: Wrong amount of cash

Some folks make the mistake of holding too little cash - they assume they can sell assets or borrow money when they need the cash. Sometimes when you most need it the window is closed or the price is painfully high.

Too much cash is a problem, too, though.

Cash Drag

Cash drag can be a huge problem for portfolios. Over the long run the value of cash, of whatever currency, goes in one direction: Down. It’s like an ice cube melting in a refrigerator – and when inflation hits the refrigerator gets unplugged.

A surprising number of investors simultaneously care a lot about investment performance but also hold entirely too much cash without a well reasoned perspective on why _that_ is the right amount of cash.

Most of the audience for this post will know that cash drag is a problem - and yet due to various behavioral barriers they’ll be sitting on too much cash. I target a specific amount of cash over time to avoid falling into this trap because I know otherwise I will demand too much of a safety blanket.

What is safe in the short term is a guaranteed problem in the long term. While I think sometimes the bear case on the dollar is a bit overdone it is true that purchasing power declines year over year – and if you look at currencies from Turkey to Nigeria you can see cases of much more rapid evaporation of value.

Cash isn’t quite as safe as it seems.

Problem 2: Yield “theft”

Some investors fall prey to what feels like a form of theft: Banks will offer them some “free” or included service or account feature in return for holding a certain amount of cash on deposit. The spread between what they could earn on a federal money market fund with similar liquidity profile is absolutely massive, often hundreds of basis points.

What’s going on here? Much of the banking industry makes their money on something called NIM or net interest margin - basically the difference between what they can earn on interest and what they pay out to their customers. You should have a clear understanding of where you’re giving up interest income and what you’re getting in exchange.

There are people who keep a lot of cash on hand in an account that yields virtually nothing, forgoing, conservatively, say $2000/yr in interest income in order to get “free ATM rebates” where they _at most_ would withdrawal cash 2x per month, pay _at most_ $10 in fees for an annual upper limit cost of $240.

At the higher end there are folks who will keep millions in subpar private bank cash accounts in order to get access to a banker who will pick up the phone. In some cases the spread is so wide that these folks could basically hire a personal assistant or full time family office staff member instead of giving the interest rate spread to the bank.

Let’s say a bank has a UHNW client with $5,000,000 on deposit, the bank can get 5.33% on the Fed’s overnight rate, they’re actually paying the client 2.33% meaning they’re pocketing 3% a year on this deposit, or $150,000 (!) / yr.

Tracking what you’re actually getting paid on your cash, benchmarking that against best-in-class options, and overcoming momentum to move to earn a better yield is one of the best ROIs most investors leave on the table.

Problem 3: Wrong bank account, wrong time

The flip side of optimizing yield is that this can push you to keep more on deposit in a country, currency, or account that pays more interest (good) but if you have obligations to be paid out in another bank country, currency, or bank account you need to make sure you’re good for it.

I’ve talked to _dozens_ of investors who ended up in some degree of distress, paying fines, or other sort of trouble because they, or someone who works for them, didn’t have the right visibility or plan on where money should be when.

For every cash reserve the key questions are:

- How quickly can I get this money into any other account?

- How do my upcoming obligations match my reserves in terms of currency?

- How diversified are my account holdings?

How quickly money can move

Some accounts like savings or checking can be accessed immediately. Others like money market funds can take at least a day to sell and clear into a bank account from which they can be routed onwards.

Especially when dealing with new accounts it can be good to double check all the entry and exit flows to see how long things actually take. Keep in mind that international transfers and/or FX can take time.

Fun fact: A lot of banks will close off the ability to send or receive international wires in certain currencies in order to force you to use their exorbitantly priced FX products. Don’t assume that all currency/transfer channels are open - or that they can’t get blocked later (see more below).

A firm like Interactive Brokers will provide FX services for between 20bps and 8bps depending on volume, and Wise will also provide a reasonably competitive service. However, many banks, especially outside the US, will charge as much as 1% or 2%.

Matching obligations and reserves on currency

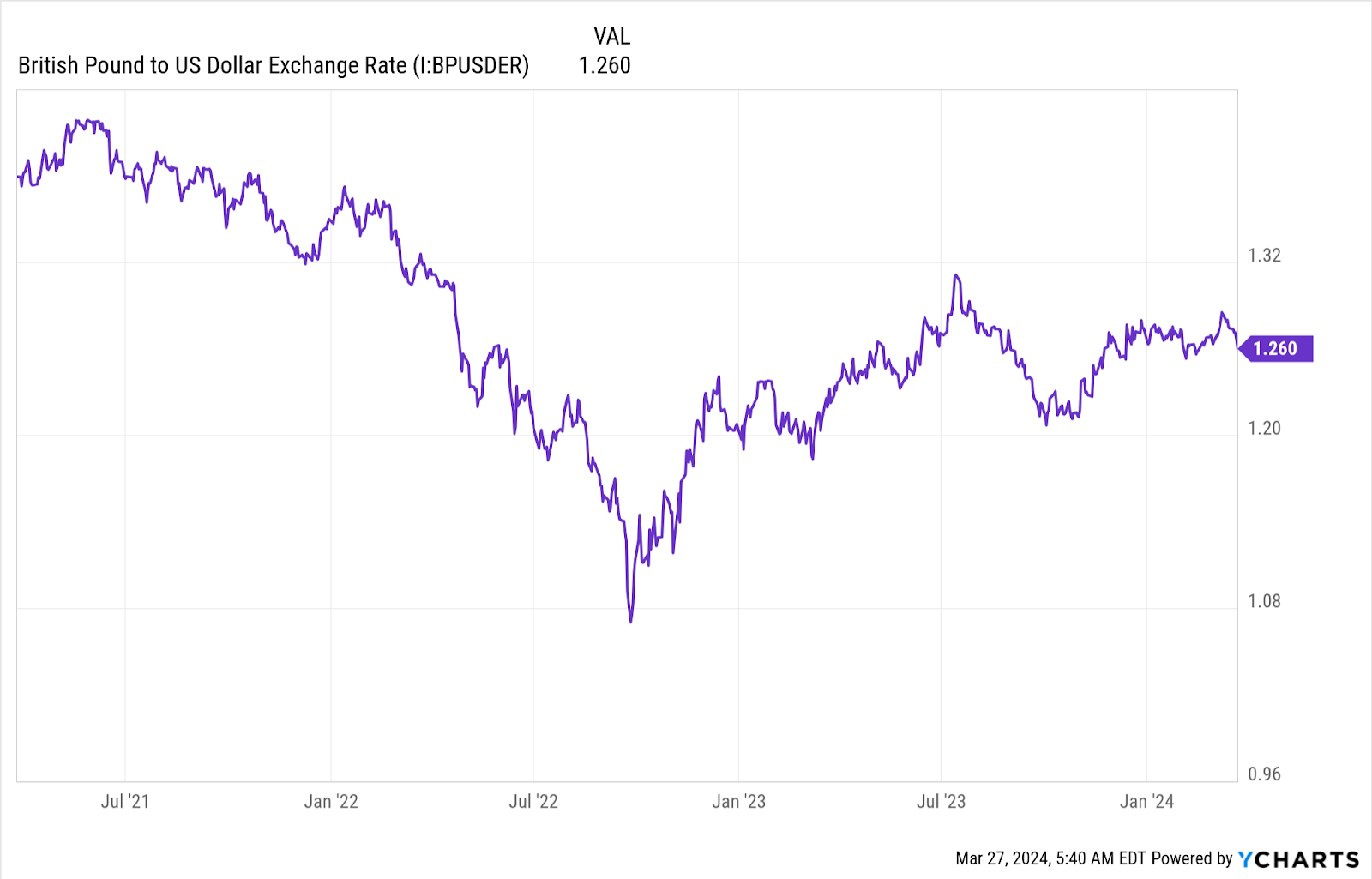

You just need to be thinking about where you may, inadvertently, be making a bet or trade on FX rates. For example, I live in Singapore and roughly half my spending is in SGD and the other half is in USD. But, most of my income is in USD. So I keep a significant SGD reserve - to keep all my reserves AND income in USD would be an implicit bet that USD will appreciate relative to SGD - which isn’t something I have conviction on.

SGD is a pretty stable currency - but even some major currencies can have huge swings - see GBP below as an example. If you owe hundreds of thousands in tax these shifts can quickly become a very big deal if you’re not properly positioned.

How diversified are my account holdings

Bank and brokerage accounts aren’t always secure or accessible. One of your accounts could be compromised. A bank could have concerns about an account and freeze the funds within it while they clear up any concerns. Banks can have IT systems go down and become temporarily inaccessible.

It’s wise to have a backup plan - there should always be more than one way to get an important payment made - more than one source of funds, more than one path to transfer or FX funds, more than one way to actually pay.

Many expats relied on Interactive Brokers for FX and money movement but they began to tighten policies on folks doing this after FINRA fined them for lax compliance on AML checks. I have friends who were caught on their financial back-foot because of this!

With a plethora of custodians, credit cards, fund transfer platforms this is straightforward to do - but does require some work. It can also make tracking everything a bit more tedious but the redundancy and reliability it provides is an obvious trade-off.

Solutions

Define an appropriate policy for each type of cash

- Working capital - These accounts tend to have the best liquidity but worst interest rate/return characteristics. Ideally you can automate sweeping cash into these accounts from higher yielding reserves and keep whatever you feel is the safe minimal buffer here.

- Operating reserves - These should be quickly accessible, not face liquidity, interest rate, or substantial credit risk - but it’s probably ok if it takes a day or so to get access to these funds. Ideally they can be automatically deployed into Working capital accounts to avoid excess drag there.

- The appropriate level of Operating reserves is a somewhat personal question regarding how much safety you’re willing to pay for. Some folks like 6mo, others feel best with a few years of expenses in a reserve.

- This choice partly depends on how much income you expect to generate from all sources over the next year or two, how uncertain that income is, and how uncertain your expenses are.

- Investing reserves - available to deploy into investment opportunities (unexpected) or meet upcoming capital calls (expected pre-committed investments)

- There are a few different reasons to hold funds in this bucket:

- There are investment opportunities you want to participate in (or have pre-committed to) that will be coming up in the future - and you want to be able to act on these quickly.

- You have an opinion about market aggregate valuations and think you can enter into investments at a better price in the future.

- You are taking some gradual deployment approach (e.g. dollar cost averaging, value averaging, etc) to avoid deploying all your capital at once for risk management or psychological reasons.

- The main thing is to be very clear about which of these reasons (or how much capital per reason) you’re holding cash for.

- Additionally - in an inverted or flat yield curve, or rising rate environment, it can make sense to use money market (essentially ultra short fixed income) as a short term replacement for fixed income/bond allocations. It’s important to note that this is a timing bet on interest rates, though and markets can pivot very quickly - see below.

- There are a few different reasons to hold funds in this bucket:

Consider where margin can plug the gap instead of cash

- If most of your cash is in a high yield vehicle (say, federal money market) it might take a few days to get that money routed to wherever you need it. A margin loan or HELOC can be a way to get cash same-day without holding too much cash in low yielding “working capital” accounts.

- These sorts of revolving credit facilities are not, in my opinion, a substitute for having the right allocation of cash overall. Rather, these are useful for plugging a “cash locality” gap in a moment of need. These days HELOCs and margin loans will have rates in the 7%-14% range - so fine for a few days, pretty destructive over a longer period of time.

Look at cash and a 12-18mo forward liquidity projection to make allocation decisions

- On the top line you’ll want to understand not just your existing cash on hand but also all the income and other sources of liquidity you expect to see in coming months.

- You’ll also need to have a basic model of all the cash that will be leaving your accounts for spending, gifts, investments, etc.

- Without the right tools, model or plans this can be labor intensive, but done properly this is actually pretty easy to do. Getting this right means never being forced to sell at a bad time, sleeping well at night knowing you’re covered, and not getting eaten by inflation and cash drag.

Getting your cash allocation and management plan in order ahead of time, planning for contingencies and potential problems, can greatly reduce stress when you most need it. Often when you need unexpected cash is the last moment you’ll want to be trying to raise it or deal with annoying technical issues with the financial system.